Which Bonds Hold Up Best During an Inflation Scare

If you invest in bonds like many retired and soon-to-be-retired investors your nightmare scenario is being loaded to the gills with long bonds when an unexpected rise in inflation strikes.

A big spike in inflation causes interest rates to rise and long-bond prices to plummet.

Why do bond prices fall when interest rates rise? When you invest in bonds, you sign up for fixed semi-annual coupon payments. For example, if you bought a 10-year Treasury bond in December 2020 for $1,000, you would have locked in a semi-annual coupon payment of about $4.50 for the next ten years.

Today, the Treasury is issuing bonds that pay $225 semi-annual coupon payments. In order for the bond with the $4.50 semi-annual coupon payment to remain competitive with today’s newly issued bonds, its price must decline.

We aren’t talking about a minor price decline either. To remain competitive, the price of that bond would have to fall to $750 today–a 25% loss three years after the initial purchase.

Bond bear markets may not be as deep as bear markets in stocks, but they can be just as nasty.

Best Performing Bonds When Inflation Soars

Okay so owning longer-term bonds when inflation unexpectedly soars can lead to major losses. Do all bonds respond similarly to rising inflation and interest rates? What are the best bonds to own when inflation rises?

Some investors think inflation-protected securities, or TIPS, are the best bonds to own when inflation rises. TIPS are Treasury bonds that provide a return by paying a real coupon rate and compensating investors for rising inflation through principal adjustments. Some view TIPS as a the only true risk-free bonds.

But are they?

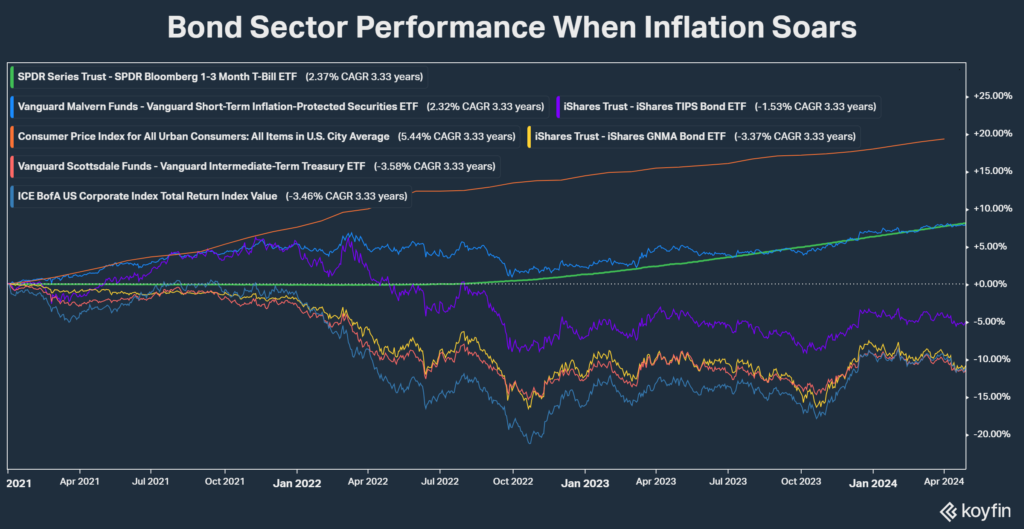

The chart below shows how TIPS and other investment-grade bond sectors performed since inflation started to rise significantly at the end of 2020.

The bond sectors included on the chart are investment-grade corporates, intermediate-term Treasuries, TIPS, short-term TIPS, GNMA mortgage securities, and T-bills. I’ve also included the CPI for comparison purposes.

Since December 31, 2020, inflation is up 19%. Intermediate-term Treasury bonds, GNMAs, and corporates are down between 10.8% and 11.4%. Deducting inflation of 19% from the 11% loss on bonds is a 30% loss in inflation-adjusted terms. Clearly these bond sectors aren’t the best place to be when inflation rises.

What about TIPS? TIPS didn’t hold up as well as one might have expected (down 5%) because they are impacted by both inflation and changes in real interest rates. TIPS initially performed well when inflation rose, but as real interest rates moved up, TIPS prices tumbled.

Short-term TIPS held up better, delivering a 7.9% return, but T-bills were the winner here with an 8.1% return. The performance of T-bills in an inflationary environment may be surprising to some, but their ultra-short maturity allows them to adjust to rising interest rates quickly.

As long as the Fed maintains credibility and raises interest rates to combat inflation, T-bills should be one of the better performers when inflation rises unexpectedly.

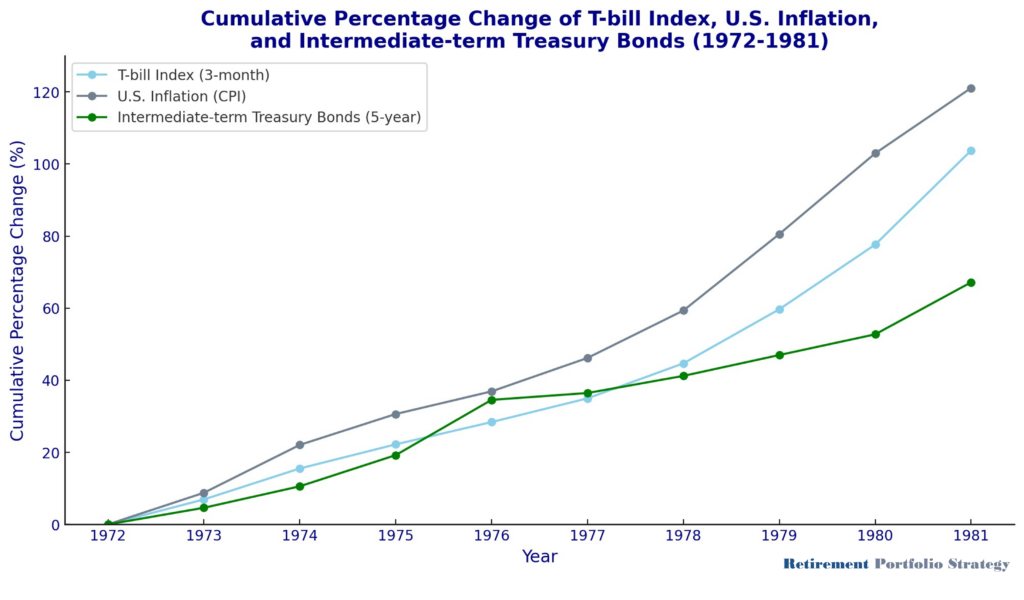

T-bills a Winner in 1970s Inflation

T-bills also held up better than longer maturity bonds during the 1970s inflation.

The chart below compares the cumulative percentage change in inflation, T-bills, and intermediate-term Treasury bonds from year-end 1972 to 1981. T-bills didn’t keep pace with inflation, but they performed better than intermediate-term Treasury bonds. Note that TIPS didn’t exist until the late 1990s, mortgage bonds were in their infancy, and corporates performed similarly to Treasuries during this period, so they are not included on the chart.

While T-bills may be your best bond bet when inflation soars, over the long-term you will want to be sure to include stocks in your portfolio. Stocks are one of the better long-term inflation hedges.