Is Apple Still a One Trick Pony?

In 2018, when iPhone unit sales were stagnating, Apple decided to stop releasing unit sales numbers to investors. Tim Cook and company said unit sales were not important. Apple wanted to convince Wall Street that it wasn’t a hardware company almost entirely reliant on the iPhone, but a services company. Services companies are valued much more highly by investors than hardware companies.

Apple’s pitch always seemed like a reach to me. When almost all services that iPhone users consume were tied directly to their iPhone, why would Wall Street put a premium multiple on the stock.

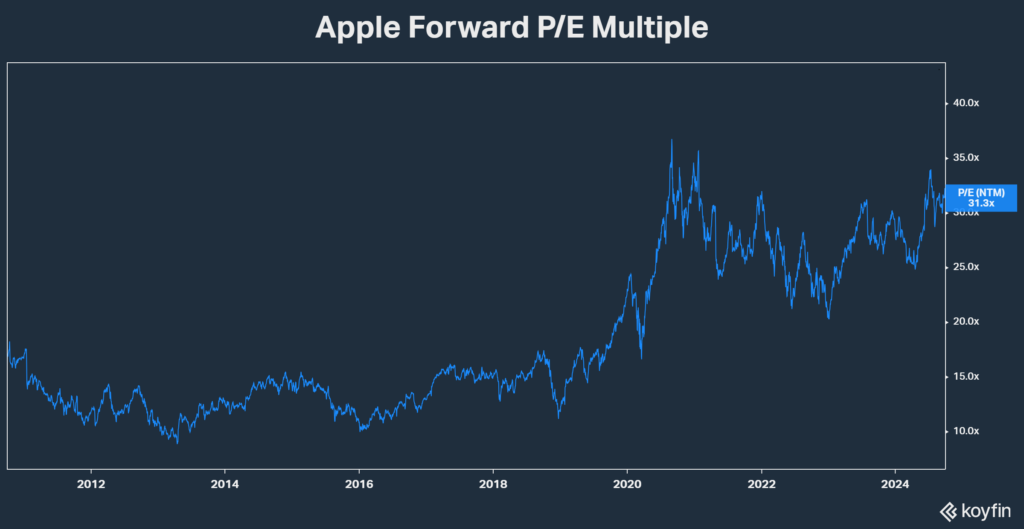

Wall Street bought what Cook was selling though. Apple’s multiple increased from about 16X before it stopped reporting unit sales to over 31X today.

The premium multiple remains even though net income has been fairly stagnant outside of a bump in demand from COVID and despite the fact that Apple remains as reliant on the iPhone as it was six years ago.

A research analyst from Needham recently pointed out just how reliant Apple is on the iPhone.

She estimates Apple could haul in $108 billion in services revenue next fiscal year, representing just over a quarter of overall revenue. And 100% of that services revenue is dependent on iPhone ownership, in her view. The services business includes various things, including streaming offerings like Apple TV+ and Apple Music, as well as insurance and the App Store.

Then there are Apple’s other products, which she expects to together generate $97 billion in revenue next fiscal year. Martin thinks that ownership of those products is highly dependent on whether consumers also have iPhones, to the extent that perhaps 50% to 80% of people would “churn out” of these other product categories if they stopped using an iPhone.

For that reason, she calculates that 89% to 96% of Apple’s revenue is linked to iPhone ownership.

Slow growth and product concentration haven’t stopped Apple shares from performing well over recent years, but at 31X earnings, there is a lot of hope priced into the stock. Hope that a formidable competitor won’t emerge, hope that AI will drive profitability, and hope that sentiment toward the stock will remain favorable.

Everything could of course turn out aces for Apple investors, but there is perhaps a lot more risk in Apple than one might assume of America’s largest stock.