Dividend Stocks vs. Retirement Stocks

Dividend stocks have long been the favored choice for retirement stock investors seeking durable businesses that offer steady income streams. Dividend stocks can make outstanding long-term investments.

Over the years, I have invested in many outstanding dividend stocks for my own portfolio and in the portfolios of clients. For over twenty years I managed a global dividend-only equity strategy for a leading investment advisory firm. If a stock didn’t pay a dividend, we didn’t buy it.

Disappearing Dividends

The trouble with pursuing a dividend-only strategy today is that the universe of attractive dividend stocks has gotten notably smaller and less relevant.

Consider this: among the top seven stocks in the S&P 500, which make up a whopping 30% of the index, the highest dividend yield is a meager 0.70% (the average is an even more pitiful 0.42%). Three of the seven don’t even pay a dividend! Looking at the top 20 stocks in the S&P 500, only two offer a dividend yield of more than 3%. These twenty stocks make up 43% of the index.

What are these companies doing with all their cash if they aren’t paying meaningful dividends?

Stock buybacks!

The unfortunate reality for high-dividend-loving investors is corporate cash distribution strategies have changed. More companies are choosing to return more of their cash flow to shareholders in the form of stock buybacks.

We can debate whether the motives behind the trend toward more buybacks are pure (count me skeptical), but there is no denying that buybacks have a major influence on stock performance. And the trend toward more buybacks shows no signs of slowing. In fact, the opposite is true.

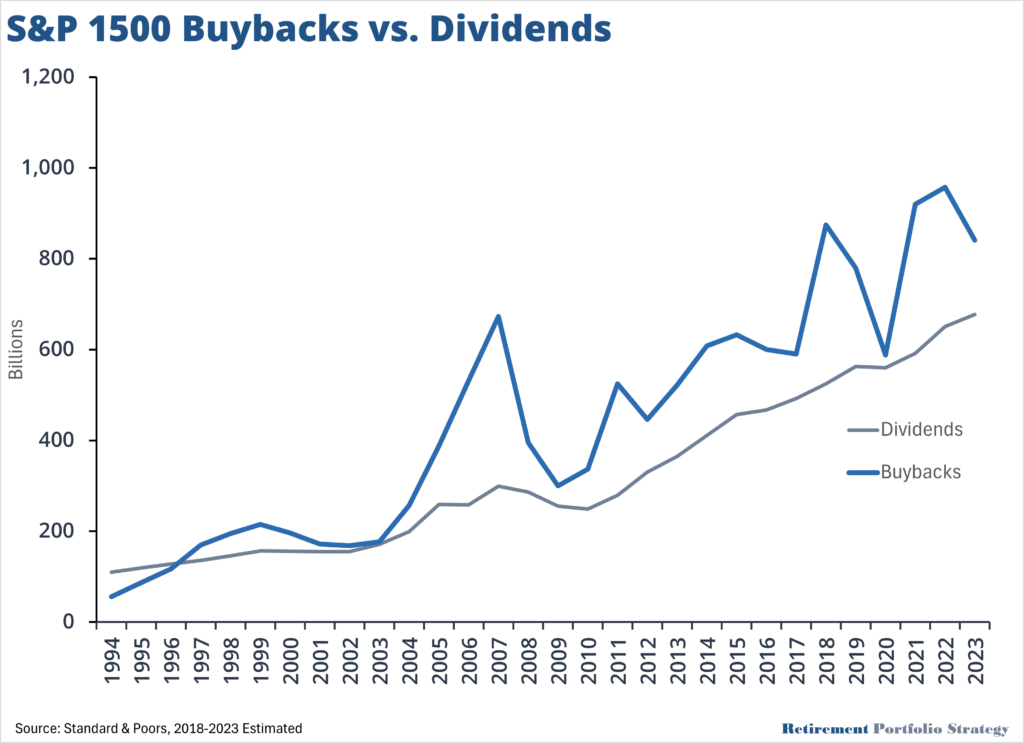

Buybacks More Prevalent than Dividends

The chart below shows the amount of cash returned to shareholders in the form of dividends and share buybacks from 1994-2023. Big U.S. companies use more of their cash buying back stock than paying dividends.

What’s more, the percentage of companies in the S&P 500 engaging in buybacks has more than doubled since the early 1990s. In 1991, less than half of S&P 500 companies had a buyback program. Today, that figure is 90%.

Good News and Bad News for Dividend-Loving Investors

The bad news for dividend-loving investors is the days of being able to craft a properly diversified portfolio of high-dividend paying stocks are likely gone for good. The good news is there is no universal law requiring you to invest your retirement money exclusively in high-dividend paying stocks. When selected with care, low and non-dividend paying stocks can make just as good, if not better, retirement stocks.

Moving Beyond a Dividend-Only Strategy

Savvy investors recognize the need to move beyond a dividend-only approach to retirement portfolio construction.

The question many have is, how do you do it without sacrificing the business quality, durability, and greater price stability that are so desirable in retirement portfolios?

Here’s how we do it at Retirement Portfolio Strategy.

The major problem with a dividend-only approach is that the universe of attractive candidates is now too narrow to craft a properly diversified portfolio. We look to solve this problem by considering a broader universe of stocks.

We start with the 1,000 largest stocks in the U.S. because bigger companies are often more established businesses with staying power.

But big doesn’t always translate into high-quality, durability, and better price stability. Enron, AIG, Lehman Brothers, Tyco, WorldCom, and countless others were big, but they still collapsed.

To reduce the chances of buying a big company that ends up on the who’s who list of Fortune 500 failures, we filter out the most speculative stocks from the list of 1,000 we start with. As a group, speculative stocks have higher risk of failure, stomach-churning sell-offs, and dismal performance.

We define speculative stocks using a composite of variables that measure quality and share price stability.

The stocks that remain after eliminating the most speculative stocks are eligible to be rated using our Retirement Stock Ratings® system. We view it as our retirement stock universe.

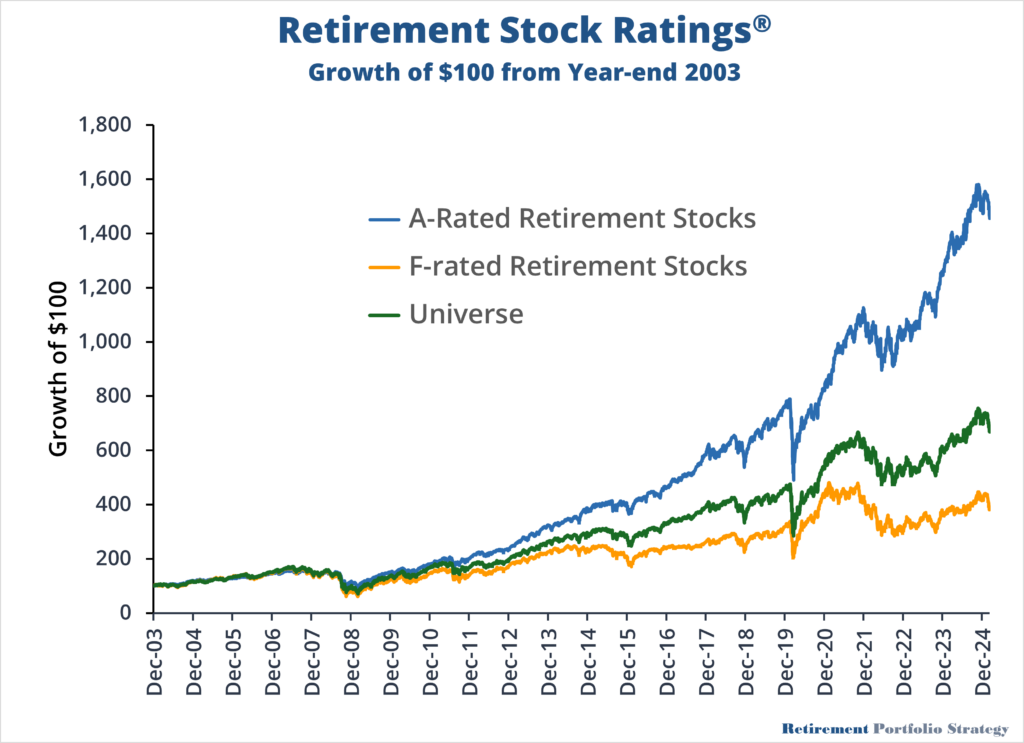

Retirement Stock Ratings®

The Retirement Stock Ratings® system evaluates all stocks in our retirement stock universe on a variety of factors we have found to result in better investment outcomes. We look at timeliness, value, shareholder yield, and sentiment, among other factors.

Each stock receives a letter grade. Just like in school, the As and Bs are desirable. The Ds and Fs should be avoided or sold.

The chart below shows the performance of the As and Fs vs. the entire 1,000 stock universe we start with. The chart assumes equal weighting and monthly rebalancing. These results are based on a simulation and do not account for transaction costs or fees.

The Retirement Stock Ratings® system offers a powerful tool for identifying the most attractive opportunities in the retirement stock universe, helping you make informed decisions and achieve your financial goals. Access to our entire database of Retirement Stock Ratings is proprietary, but we reference our ratings for specific stocks in many posts on this site.